Academic research refers to the persistent phenomenon of ex-post implied volatility (IV) exceeding realized volatility (HV) as the Volatility Risk Premium (VRP). As it applies to option premiums, this leads to a positive expected return for being a systematic option seller.

This can be seen in historical market data, and from an efficient markets point of view, should be expected to persist in the future as a rational risk premium for the transfer of risk from a willing buyer to a willing seller.

Stop and think with me for a moment about the concept of passive vs. active. I believe it's wise to only invest in strategies ("factors") with an underlying expected return, before any active management is applied. In other words, the market naturally makes you money over time without any requirement of an investment manager's "skill" to be able to select securities and/or time entries and exits. This is important because academic research has documented manager skill in decades of historical mutual fund performance to exist less than would even be randomly expected (especially after fees and taxes).

WE RECOMMEND THE VIDEO: Binary Trading Biggest fraud Revealed with Live proof | Big Youtubers make you fool | Binary Scam

hello guys from this video I am going to show you how binary trading apps like binomo, olymtrade, iq option, expert option and others doing scam with you and ...

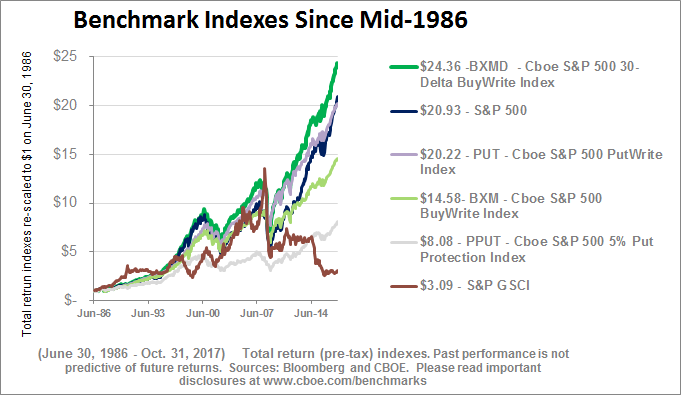

As an example of a passively managed VRP strategy, the CBOE has been publishing their S&P 500 Put write index for years, with historical data going back to 1986. Since then, a passive strategy of selling fully cash secured one-month at the money (ATM) S&P 500 puts, with collateral assumed to be held in a money market account holding US Treasury bills, would have produced returns similar to the S&P 500 index itself. Due to the nature of ATM puts, risk (measured as volatility and drawdown) was less than the underlying index, resulting in about a 30% increase in Sharpe Ratio.

Put selling is robust across markets as well, as can also been seen in CBOE's historical data for PUTR, where the same methodology is applied to the Russell 2000 index. With liquid option markets on ETF's like EFA and EEM, a globally diversified equity put write strategy could be constructed with attractive characteristics vs. a traditional mutual fund or ETF that only holds the underlying equities. (Readers can backtest these ideas for free for an entire week with a free trial of the highly recommended ORATS Wheel)

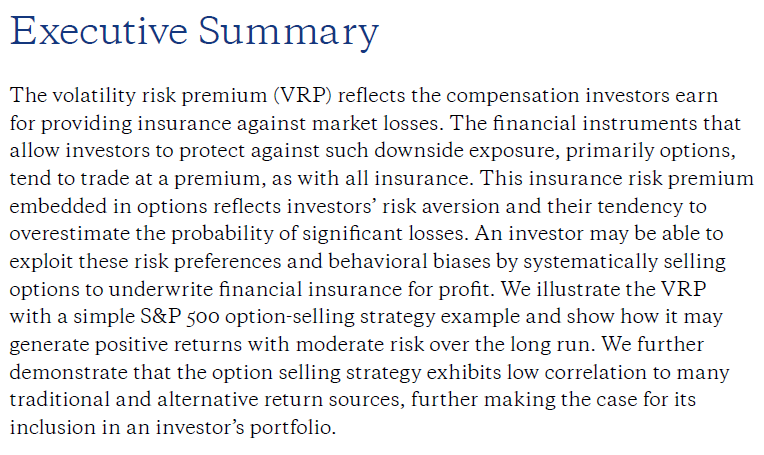

Last month, AQR published an excellent paper, Understanding the Volatility Risk Premium. The paper's executive summary is presented below:

The authors also present an interesting case study of how investor behavior tends to create significant demand for and value placed on insurance like investments, such as buying puts to hedge a position or portfolio. These preferences and behavioral biases cause an overestimation of downside risk, documented by a Yale University survey conducted where both retail and institutional investors were asked to estimate the probability of a "catastrophic stock market crash" within the next six months. Since 1989, with few exceptions, a majority of both groups consistently believe that there is a greater than 10% chance of such, yet in reality the historical likelihood of such an event has been approximately 1%. This overestimation of crash risk may be part of the explanation of the persistent VRP seen in option and volatility futures pricing where option and volatility futures buyers are willing to pay, and sellers require receipt, of a large premium to transfer risk from one party to another.

On the opposite end of the option spectrum is call options, where the VRP has also been documented to exist (and can be seen in CBOE's BXMD index in the chart above), although for slightly different reasons. Call options can be thought of as lottery tickets, where a buyer spends a small amount of money to have the potential for a large payoff if the underlying asset moves much farther and faster to the upside than the market expected. This preference for positive skew results in a call option VRP that can also be captured by option sellers in a variety of different ways, including covered calls and short strangles where short puts and calls are combined into one (usually) delta neutral position.

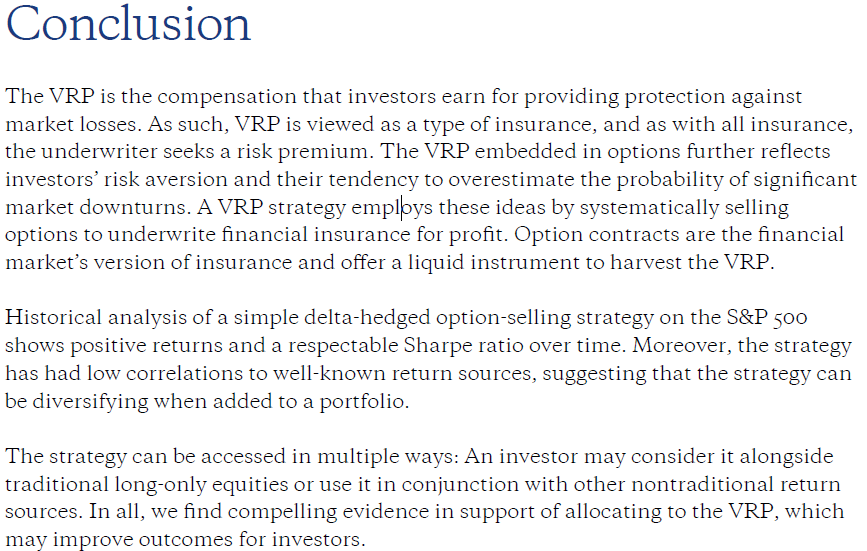

I'll finish with the conclusion from AQR's paper, but before I do, a word of caution. The reason you often hear "options are risky" is because people often are under-educated about the inherent leverage built into options. Remember, one contract is the equivalent of 100 shares of the underlying. Don't rely on your broker's margin requirement as any indication of how many contracts you should sell any more than you'd rely on a sports car's ability to drive 180 MPH as any indication of how fast you should drive. In our firm, we believe that any skill that may persist in financial markets is in having a deep understanding of portfolio construction, and then the discipline to have a long term mindset when most others don't.

Jesse Blom is a licensed investment advisor and Vice President of Lorintine Capital, LP . He provides investment advice to clients all over the United States and around the world. Jesse has been in financial services since 2008 and is a CERTIFIED FINANCIAL PLANNER™ professional . Working with a CFP® professional represents the highest standard of financial planning advice. Jesse has a Bachelor of Science in Finance from Oral Roberts University. Jesse oversees the LC Diversified forum and contributes to the Steady Condors newsletter.

What Is SteadyOptions?

Full Trading Plan

Complete Portfolio Approach

Diversified Options Strategies

Exclusive Community Forum

Steady And Consistent Gains

High Quality Education

Risk Management, Portfolio Size

Performance based on real fills

Non-directional Options Strategies

10-15 trade Ideas Per Month

Targets 5-7% Monthly Net Return

Recent Articles

Articles

Pricing Models and Volatility Problems

Most traders are aware of the volatility-related problem with the best-known option pricing model, Black-Scholes. The assumption under this model is that volatility remains constant over the entire remaining life of the option.

By Michael C. Thomsett, August 16

- Added byMichael C. Thomsett

- August 16

Option Arbitrage Risks

Options traders dealing in arbitrage might not appreciate the forms of risk they face. The typical arbitrage position is found in synthetic long or short stock. In these positions, the combined options act exactly like the underlying. This creates the arbitrage.

By Michael C. Thomsett, August 7

- Added byMichael C. Thomsett

- August 7

Why Haven't You Started Investing Yet?

You are probably aware that investment opportunities are great for building wealth. Whether you opt for stocks and shares, precious metals, forex trading, or something else besides, you could afford yourself financial freedom. But if you haven't dipped your toes into the world of investing yet, we have to ask ourselves why.

By Kim, August 7

- Added byKim

- August 7

Historical Drawdowns for Global Equity Portfolios

Globally diversified equity portfolios typically hold thousands of stocks across dozens of countries. This degree of diversification minimizes the risk of a single company, country, or sector. Because of this diversification, investors should be cautious about confusing temporary declines with permanent loss of capital like with single stocks.

By Jesse, August 6

- Added byJesse

- August 6

Types of Volatility

Are most options traders aware of five different types of volatility? Probably not. Most only deal with two types, historical and implied. All five types (historical, implied, future, forecast and seasonal), deserve some explanation and study.

By Michael C. Thomsett, August 1

- Added byMichael C. Thomsett

- August 1

The Performance Gap Between Large Growth and Small Value Stocks

Academic research suggests there are differences in expected returns among stocks over the long-term. Small companies with low fundamental valuations (Small Cap Value) have higher expected returns than big companies with high valuations (Large Cap Growth).

By Jesse, July 21

- Added byJesse

- July 21

How New Traders Can Use Trade Psychology To Succeed

People have been trying to figure out just what makes humans tick for hundreds of years. In some respects, we’ve come a long way, in others, we’ve barely scratched the surface. Like it or not, many industries take advantage of this knowledge to influence our behaviour and buying patterns.

- Added byKim

- July 21

A Reliable Reversal Signal

Options traders struggle constantly with the quest for reliable reversal signals. Finding these lets you time your entry and exit expertly, if you only know how to interpret the signs and pay attention to the trendlines. One such signal is a combination of modified Bollinger Bands and a crossover signal.

By Michael C. Thomsett, July 20

- Added byMichael C. Thomsett

- July 20

Premium at Risk

Should options traders consider “premium at risk” when entering strategies? Most traders focus on calculated maximum profit or loss and breakeven price levels. But inefficiencies in option behavior, especially when close to expiration, make these basic calculations limited in value, and at times misleading.

By Michael C. Thomsett, July 13

- Added byMichael C. Thomsett

- July 13

Diversified Leveraged Anchor Performance

In our continued efforts to improve the Anchor strategy, in April of this year we began tracking a Diversified Leveraged Anchor strategy, under the theory that, over time, a diversified portfolio performs better than an undiversified portfolio in numerous metrics. Not only does overall performance tend to increase, but volatility and drawdowns tend to decrease: